1. Leverage the “Weekly Update” Cycle

Under the new RBI mandate, banks now report data more frequently (5 times a month).

- The Strategy: If you have a high credit card balance, pay it off at least 3 days before the next weekly reporting date (usually the 7th, 14th, 21st, or 28th of the month).

- The Result: Instead of waiting 45 days for your score to rise, you could see a jump in your CIBIL profile within 7–10 days.

2. The 30% Utilization “Golden Rule”

Your Credit Utilization Ratio (CUR) is the percentage of your credit limit you actually use. Using 90% of your limit makes you look “credit hungry.”

- Quick Fix: Keep your total usage below 30%. If your limit is ₹1,00,000, never let the balance exceed ₹30,000.

- Pro Tip: If you can’t reduce spending, ask your bank for a limit increase. This instantly lowers your utilization ratio without you having to pay a paisa.

3. Fix “Data Mismatches” Immediately

With the 2026 push for Central KYC (CKYC) integration, even a small spelling mistake in your name or a different phone number across banks can create “ghost” accounts or duplicate entries that drag down your score.

- Action: Check your CIBIL report for any loans you didn’t take or “Late” marks on bills you paid.

- Timeline: Raising a dispute online at the CIBIL portal now sees faster resolution due to stricter RBI timelines for credit bureaus.

4. Build History with a “Secured” Credit Card

If you have a low score or no history, getting a standard loan is nearly impossible.

- The Shortcut: Open a Fixed Deposit (FD) backed credit card (available with banks like IDFC FIRST, Kotak, or Axis).

- Why it works: These are 100% approved regardless of your score. Use it for small UPI-on-Credit transactions and pay it back weekly. This builds a “repayment track record” in record time.

5. Never “Settle”—Always “Close”

If you have old debt, avoid the “Settlement” trap. A “Settled” status on your report is a red flag that stays for 7 years.

- The Move: Negotiate with the bank to pay the Full Due amount in exchange for a “Closed” or “No Dues Certificate” (NDC). A “Closed” account is viewed far more favourably by 2026 lending algorithms.

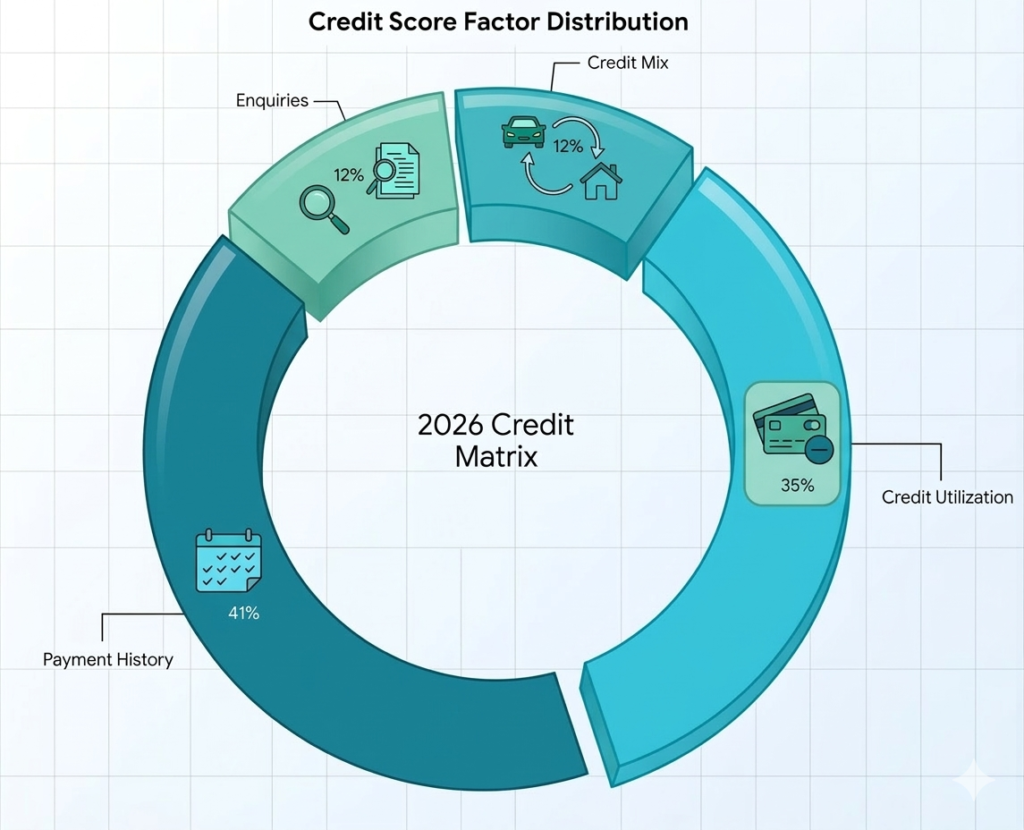

📊 Quick Summary: The 2026 Credit Score Matrix

| Factor | Impact | 2026 Speed Hack |

| Payment History | 35% | Set “Auto-Pay” to trigger 5 days before the due date. |

| Credit Utilization | 30% | Pay mid-month to keep reported balance under 30%. |

| Credit Mix | 10% | Don’t just have Credit Cards; a small Consumer Durable loan helps. |

| Enquiries | 10% | Use “Soft Search” tools to check eligibility; avoid multiple “Hard” hits. |

⚠️ Mistakes to Avoid

- Closing Old Cards: Don’t close your oldest credit card even if you don’t use it. The “age” of your credit account accounts for 15% of your score.

- Multiple Applications: Applying for 3 credit cards in one week will tank your score. Space applications by at least 3–6 months.