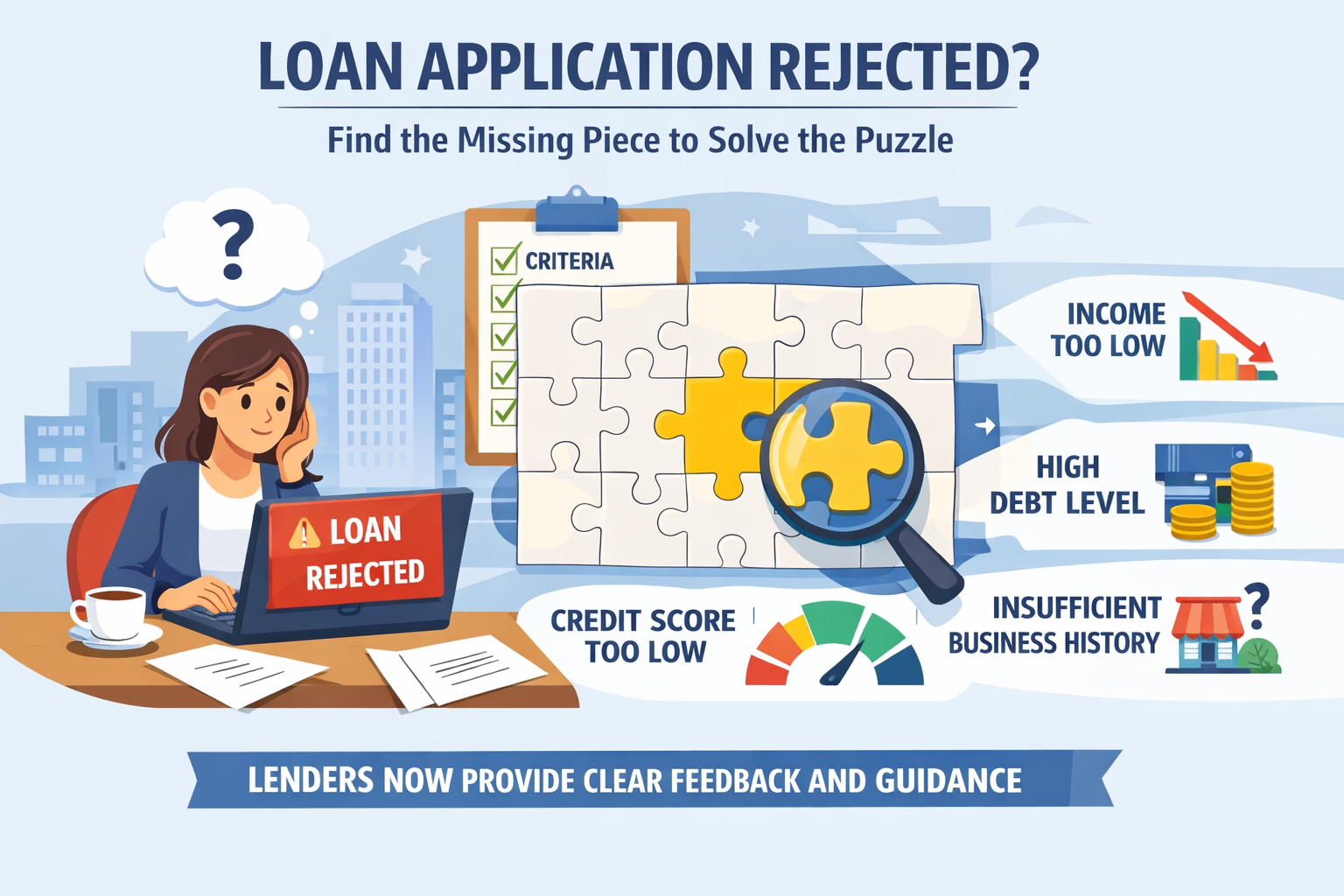

Getting a “rejected” notification on a loan application can feel like a personal setback, but in 2026’s data-driven lending environment, it’s usually just a puzzle with a missing piece. Whether you’re applying for a personal loan or a business credit line, lenders are more transparent than ever about what they’re looking for.

Here are the top reasons why loan applications get rejected and—more importantly—how you can fix them.

1. The “Invisible” or Low Credit Score

Your credit score remains the first gatekeeper. In 2026, most lenders look for a score of 750 or above for instant approval.

- The Problem: Late payments, high credit card utilization (using more than 30% of your limit), or simply having no credit history at all (“thin file”).

- The Fix: Check your report for errors. If you have no history, start small with a “secured” credit card or a consumer durable loan (like financing a phone) to build a paper trail.

2. High Debt-to-Income Ratio (DTI)

Lenders don’t just care about how much you make; they care about how much you have left.

- The Problem: If 50% or more of your monthly income is already swallowed by existing EMIs, lenders see you as “overleveraged.” They worry a new loan will be the straw that breaks the camel’s back.

- The Fix: Pay off smaller debts or credit card balances before applying for a major loan. Aim to keep your total debt obligations under 40% of your gross income.

3. “Credit Hunger” (Multiple Hard Inquiries)

Every time you hit “Apply,” a “hard inquiry” is logged on your credit report.

- The Problem: Applying to five different banks in one week makes you look desperate or financially unstable. In the eyes of an algorithm, “Credit Hungry” equals “High Risk.”

- The Fix: Use “soft search” eligibility checkers first. These tell you your chances of approval without leaving a mark on your credit report.

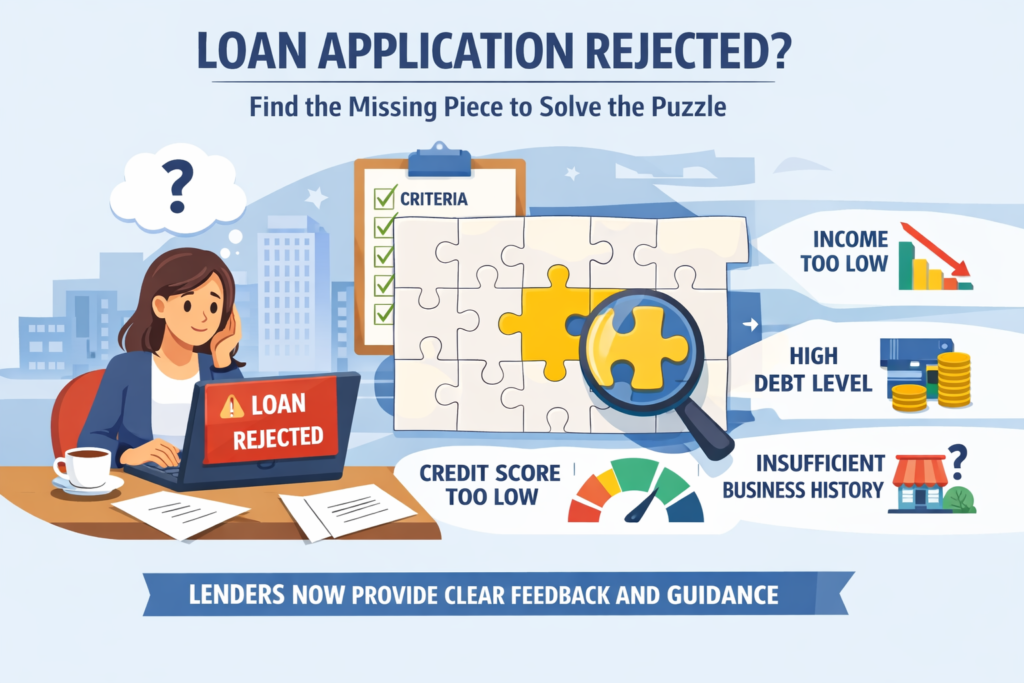

4. Unstable Employment or “Risky” Industry

Lenders love predictability.

- The Problem: If you’ve switched jobs three times in the last year or are still in a “probation period,” lenders may hit the pause button. For business loans, certain industries (like restaurants or new tech startups) are often flagged as high-risk.

- The Fix: Try to show at least 6–12 months of steady employment with your current employer before applying. If you’re self-employed, ensure you have at least two years of consistent tax returns (ITR).

5. The “Paperwork” Trap

Even with a perfect score, a typo can sink you.

- The Problem: Mismatched addresses between your ID and your application, outdated tax filings, or blurry digital uploads are common (and avoidable) reasons for instant rejection.

- The Fix: Double-check that your name and address are identical across your PAN, Aadhaar (or local ID), and bank statements. In 2026, digital verification is instant—accuracy is non-negotiable.

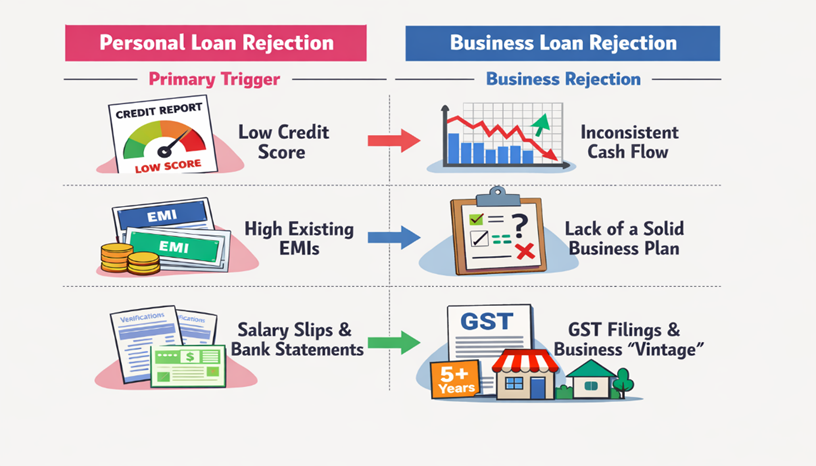

Comparison: Personal vs. Business Rejections

| Feature | Personal Loan Rejection | Business Loan Rejection |

| Primary Trigger | Low personal credit score | Inconsistent cash flow |

| Common Culprit | High existing EMIs | Lack of a solid business plan |

| Verification | Salary slips & Bank statements | GST filings & Business “vintage” |

What to do if you get rejected?

Don’t panic and—critically—don’t apply again immediately.

1. Ask why: Lenders are often required to give a specific reason for rejection.

2. Wait 3–6 months: Give your credit score time to recover from the inquiry.

3. Correct the issue: Whether it’s closing an old credit card or updating your address, fix the root cause first.