When you need quick access to funds—whether for an emergency, a big purchase, or debt consolidation—you’ll often face two popular options: a personal loan or a credit card loan. While both provide access to credit, they differ significantly in terms of cost, flexibility, and usage. Understanding these differences can help you make a smarter financial decision.

What is a Personal Loan?

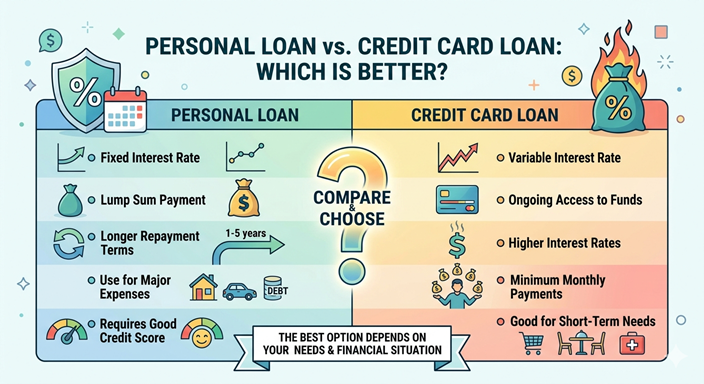

A personal loan is a type of unsecured loan offered by banks and financial institutions. You receive a lump sum amount upfront and repay it in fixed monthly installments (EMIs) over a predetermined tenure.

Key Features:

- Fixed interest rates (usually lower than credit cards)

- Fixed repayment tenure (1–5 years typically)

- Higher loan amounts

- Predictable monthly payments

What is a Credit Card Loan?

A credit card loan (also called a loan on credit card) allows you to borrow money against your credit limit. It can be taken as:

- Cash advance, or

- Convert-to-EMI option on existing credit card transactions

Key Features:

- Quick approval with minimal paperwork

- Higher interest rates

- Shorter repayment tenure

- Limited loan amount (based on your credit limit)

Personal Loan vs Credit Card Loan: Key Differences

| Feature | Personal Loan | Credit Card Loan |

| Interest Rate | Lower (10%–18%) | Higher (18%–36% or more) |

| Loan Amount | Higher (₹50,000 to ₹25 lakh+) | Limited to credit limit |

| Tenure | Longer (1–5 years) | Shorter (3–36 months) |

| Approval Time | Moderate | Instant or very fast |

| Repayment Flexibility | Fixed EMIs | Flexible but costly |

| Best For | Large expenses | Short-term needs |

When Should You Choose a Personal Loan?

A personal loan is generally better if:

- You need a large amount of money

- You want lower interest rates

- You prefer structured repayment

- You are planning debt consolidation

👉 Example: Medical emergencies, weddings, home renovation

When Should You Choose a Credit Card Loan?

A credit card loan works better if:

- You need instant funds

- The amount required is small

- You can repay quickly

- You want no documentation hassles

👉 Example: Urgent travel, small unexpected expenses

Pros and Cons

Personal Loan

Pros:

- Lower interest cost

- Fixed repayment plan

- Suitable for large expenses

Cons:

- Approval may take time

- Requires documentation

Credit Card Loan

Pros:

- Instant availability

- Minimal paperwork

- Convenient

Cons:

- Very high interest rates

- Risk of debt trap if mismanaged

Which One is Better?

There is no one-size-fits-all answer.

- Choose a personal loan if you want affordability and stability.

- Choose a credit card loan if you need speed and convenience for short-term borrowing.

👉 Rule of Thumb:

If you cannot repay quickly, avoid credit card loans due to high interest.

Final Thoughts

Both personal loans and credit card loans serve different financial needs. The right choice depends on your urgency, repayment capacity, and the loan amount required. Always compare interest rates, read the fine print, and borrow responsibly to avoid unnecessary financial stress.

Bonus Tip 💡

Before taking any loan:

- Check your credit score

- Compare offers from multiple lenders

- Calculate total repayment cost (not just EMI)

Making an informed decision today can save you significant money in the long run.